Medicare will help cover some of your healthcare costs in retirement, but choosing the right option can be difficult. Review the basics to find out which coverage option is right for you.

5 min read | February 08, 2019

Once you reach age 65, Medicare will help cover some of your healthcare costs in retirement. But like Social Security, choosing the right Medicare option can be difficult. The video above has a quick overview of the basics and helps explain how to pick a Medicare coverage option.

You usually don’t pay a monthly premium for Medicare Part A coverage if you or your spouse paid Medicare taxes while working. This is sometimes called “premium-free Part A.”

Premiums for Medicare Part B vary depending on your household income. Remember, deadlines are one of the most important things to know and can impact your cost. If you don’t enroll when you’re first eligible, premiums will increase 10% for each full 12 months until you do enroll.

If your yearly income in 2019 (for what you pay in 2021) was:

| File individual tax return | File joint tax return | File married & separate tax returm | You pay each month (in 2021) |

|---|---|---|---|

| $88,000 or less | $176,000 or less | $85,000 or less | $148.50 |

| Above $88,001 up to $111,000 | Above $176,001 up to $222,000 | N/A | $207.90 |

| Above $111,001 up to $138,000 | Above $222,001 up to $276,000 | N/A | $297.00 |

| Above $138,001 up to $165,000 | Above $276,001 up to $330,000 | N/A | $386.10 |

| Above $165,001 up to $500,000 | Above $330,001 to $750,000 | above $85,000 and less than $415,000 | $475.20 |

| $500,000 or above | $750,000 and above | $415,000 and above | $505.90 |

Known as Medicare Advantage, plans are provided by private companies and can vary quite a bit from one plan to another. By law, they must at least be equivalent to regular Parts A and B coverage. But some Medicare Advantage plans provide greater coverage than Parts A and B.

Carefully compare how each Medicare Advantage plan stacks up to the costs and benefits of original Medicare. The Medicare Plan Finder at medicare.gov can help.

Cost for Medicare Part D will depend on which plan you choose, and it may incur an additional charge depending upon your income.

If your filing status and yearly income in 2019 was:

| File individual tax return | File joint tax return | You pay each month (in 2020) |

|---|---|---|

| $88,000 or less | $176,000 or less | Your plan premium |

| Above $88,001 up to $111,000 | Above $176,001 up to $222,000 | $12.30 + your plan premium |

| Above $111,001 up to $138,000 | Above $222,001 up to $276,000 | $31.80 + your plan premium |

| Above $138,001 up to $165,000 | Above $276,001 up to $330,000 | $51.20 + your plan premium |

| Above $165,001 and up to $500,000 | Above $330,001 up to $750,000 | $70.70 + your plan premium |

| $500,000 or above | $750,000 and above | $77.10 + your plan premium |

Part D coverage can also be purchased through a stand-alone prescription drug plan offered by an outside provider, but costs will vary based on the plan you choose. You can change your plan during the Annual Coordinated Election Period (October 15 to December 7 each year). You may have to pay a penalty if you don’t apply for coverage when first eligible.

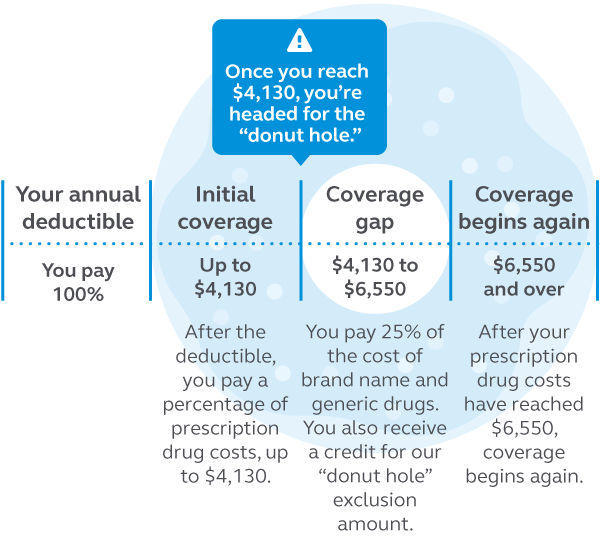

One thing you need to consider with Part D is what’s called the “donut hole.”

This diagram illustrates how this coverage gap affects most Part D programs. This means that after total retail costs for your prescriptions reach $4,130 (for 2021), you’ll have to pay the full amount until you’ve reached the out-of-pocket spending limit (up to $6,550 in 2021).

You get these savings if you buy your prescriptions at a pharmacy or order them through the mail. Some plans may offer higher savings in the coverage gap. The discount will come off the price that your plan has set with the pharmacy for that specific drug.

Although you’ll pay no more than 25% of the price for the brand-name drug in 2021, 75% of the price—what you pay plus the 70% manufacturer discount payment—will count as out-of-pocket costs, which will help you get out of the coverage gap.

These items aren’t counted toward your out-of-pocket spending:

For more information, visit medicare.gov.

Once you have reviewed how Medicare works and you understand your options, it’s time to create a plan to pay for out-of-pocket health care costs during retirement and enroll in Medicare.

When you’re ready to enroll, you’ll need to work with the Social Security Administration, which handles Medicare eligibility and enrollment. You may contact the Social Security Administration at 800-772-1213 to enroll or to ask questions about your eligibility. You can also enroll online at medicare.gov.

As a reminder, you’re eligible for Medicare when you turn 65. You don’t have to be retired or collecting Social Security to sign up, and you can do so during any of these enrollment periods:

| Initial enrollment period | Age 65 (3 months before through 3 months after) |

|---|---|

| General enrollment period | January 1 through March 31 each year |

| Open enrollment period | October 15 through December 7 each year |

| Special enrollment period | Extending up to 8 months after your group coverage ends |

There are certain times of year when you can change your existing Medicare coverage. For most people, you can change your coverage during the annual enrollment period from October 15 through December 7.

Under certain circumstances you may qualify for a Special Enrollment Period (SEP). These circumstances include:

If you or your spouse is still working and has insurance through your employer, contact your benefits administrator to find out how your insurance works with Medicare. Each situation is individual to the kind of health insurance you have.

Picking an option and enrolling in Medicare can be confusing and stressful. But you’re well on your way—just take it one step at a time.